Kernel Weights

kweights.RdKernel weights for kernel-based heteroscedasticity and autocorrelation consistent (HAC) covariance matrix estimators as introduced by Andrews (1991).

kweights(x, kernel = c("Truncated", "Bartlett", "Parzen",

"Tukey-Hanning", "Quadratic Spectral"), normalize = FALSE)Arguments

- x

numeric.

- kernel

a character specifying the kernel used. All kernels used are described in Andrews (1991).

- normalize

logical. If set to

TRUEthe kernels are normalized as described in Andrews (1991).

Value

Value of the kernel function at x.

References

Andrews DWK (1991). “Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation.” Econometrica, 59, 817--858.

See also

Examples

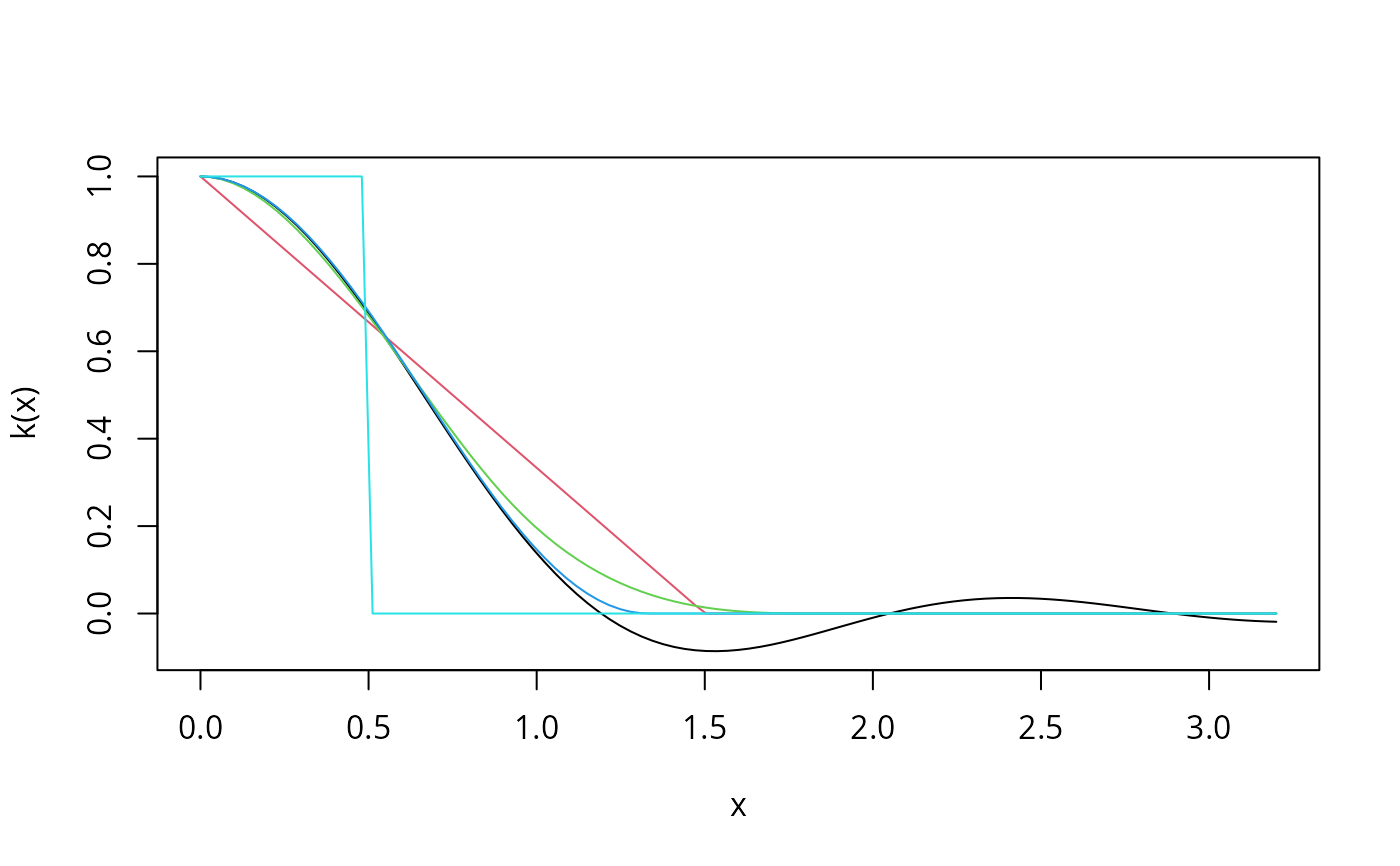

curve(kweights(x, kernel = "Quadratic", normalize = TRUE),

from = 0, to = 3.2, xlab = "x", ylab = "k(x)")

curve(kweights(x, kernel = "Bartlett", normalize = TRUE),

from = 0, to = 3.2, col = 2, add = TRUE)

curve(kweights(x, kernel = "Parzen", normalize = TRUE),

from = 0, to = 3.2, col = 3, add = TRUE)

curve(kweights(x, kernel = "Tukey", normalize = TRUE),

from = 0, to = 3.2, col = 4, add = TRUE)

curve(kweights(x, kernel = "Truncated", normalize = TRUE),

from = 0, to = 3.2, col = 5, add = TRUE)