Kernel-based HAC Covariance Matrix Estimation

weightsAndrews.RdA set of functions implementing a class of kernel-based heteroscedasticity and autocorrelation consistent (HAC) covariance matrix estimators as introduced by Andrews (1991).

kernHAC(x, order.by = NULL, prewhite = 1, bw = bwAndrews,

kernel = c("Quadratic Spectral", "Truncated", "Bartlett", "Parzen", "Tukey-Hanning"),

approx = c("AR(1)", "ARMA(1,1)"), adjust = TRUE, diagnostics = FALSE,

sandwich = TRUE, ar.method = "ols", tol = 1e-7, data = list(), verbose = FALSE, ...)

weightsAndrews(x, order.by = NULL, bw = bwAndrews,

kernel = c("Quadratic Spectral", "Truncated", "Bartlett", "Parzen", "Tukey-Hanning"),

prewhite = 1, ar.method = "ols", tol = 1e-7, data = list(), verbose = FALSE, ...)

bwAndrews(x, order.by = NULL, kernel = c("Quadratic Spectral", "Truncated",

"Bartlett", "Parzen", "Tukey-Hanning"), approx = c("AR(1)", "ARMA(1,1)"),

weights = NULL, prewhite = 1, ar.method = "ols", data = list(), ...)Arguments

- x

a fitted model object. For

bwAndrewsit can also be a score matrix (as returned byestfun) directly.- order.by

Either a vector

zor a formula with a single explanatory variable like~ z. The observations in the model are ordered by the size ofz. If set toNULL(the default) the observations are assumed to be ordered (e.g., a time series).- prewhite

logical or integer. Should the estimating functions be prewhitened? If

TRUEor greater than 0 a VAR model of orderas.integer(prewhite)is fitted viaarwith method"ols"anddemean = FALSE. The default is to use VAR(1) prewhitening.- bw

numeric or a function. The bandwidth of the kernel (corresponds to the truncation lag). If set to to a function (the default is

bwAndrews) it is adaptively chosen.- kernel

a character specifying the kernel used. All kernels used are described in Andrews (1991).

- approx

a character specifying the approximation method if the bandwidth

bwhas to be chosen bybwAndrews.- adjust

logical. Should a finite sample adjustment be made? This amounts to multiplication with \(n/(n-k)\) where \(n\) is the number of observations and \(k\) the number of estimated parameters.

- diagnostics

logical. Should additional model diagnostics be returned? See

vcovHACfor details.- sandwich

logical. Should the sandwich estimator be computed? If set to

FALSEonly the middle matrix is returned.- ar.method

character. The

methodargument passed toarfor prewhitening (only, not for bandwidth selection).- tol

numeric. Weights that exceed

tolare used for computing the covariance matrix, all other weights are treated as 0.- data

an optional data frame containing the variables in the

order.bymodel. By default the variables are taken from the environment which the function is called from.- verbose

logical. Should the bandwidth parameter used be printed?

- ...

further arguments passed to

bwAndrews.- weights

numeric. A vector of weights used for weighting the estimated coefficients of the approximation model (as specified by

approx). By default all weights are 1 except that for the intercept term (if there is more than one variable).

Details

kernHAC is a convenience interface to vcovHAC using

weightsAndrews: first a weights function is defined and then vcovHAC

is called.

The kernel weights underlying weightsAndrews

are directly accessible via the function kweights and require

the specification of the bandwidth parameter bw. If this is not specified

it can be chosen adaptively by the function bwAndrews (except for the

"Truncated" kernel). The automatic bandwidth selection is based on

an approximation of the estimating functions by either AR(1) or ARMA(1,1) processes.

To aggregate the estimated parameters from these approximations a weighted sum

is used. The weights in this aggregation are by default all equal to 1

except that corresponding to the intercept term which is set to 0 (unless there

is no other variable in the model) making the covariance matrix scale invariant.

Further details can be found in Andrews (1991).

The estimator of Newey & West (1987) is a special case of the class of estimators

introduced by Andrews (1991). It can be obtained using the "Bartlett"

kernel and setting bw to lag + 1. A convenience interface is

provided in NeweyWest.

Value

kernHAC returns the same type of object as vcovHAC

which is typically just the covariance matrix.

weightsAndrews returns a vector of weights.

bwAndrews returns the selected bandwidth parameter.

References

Andrews DWK (1991). “Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation.” Econometrica, 59, 817--858.

Newey WK & West KD (1987). “A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix.” Econometrica, 55, 703--708.

See also

Examples

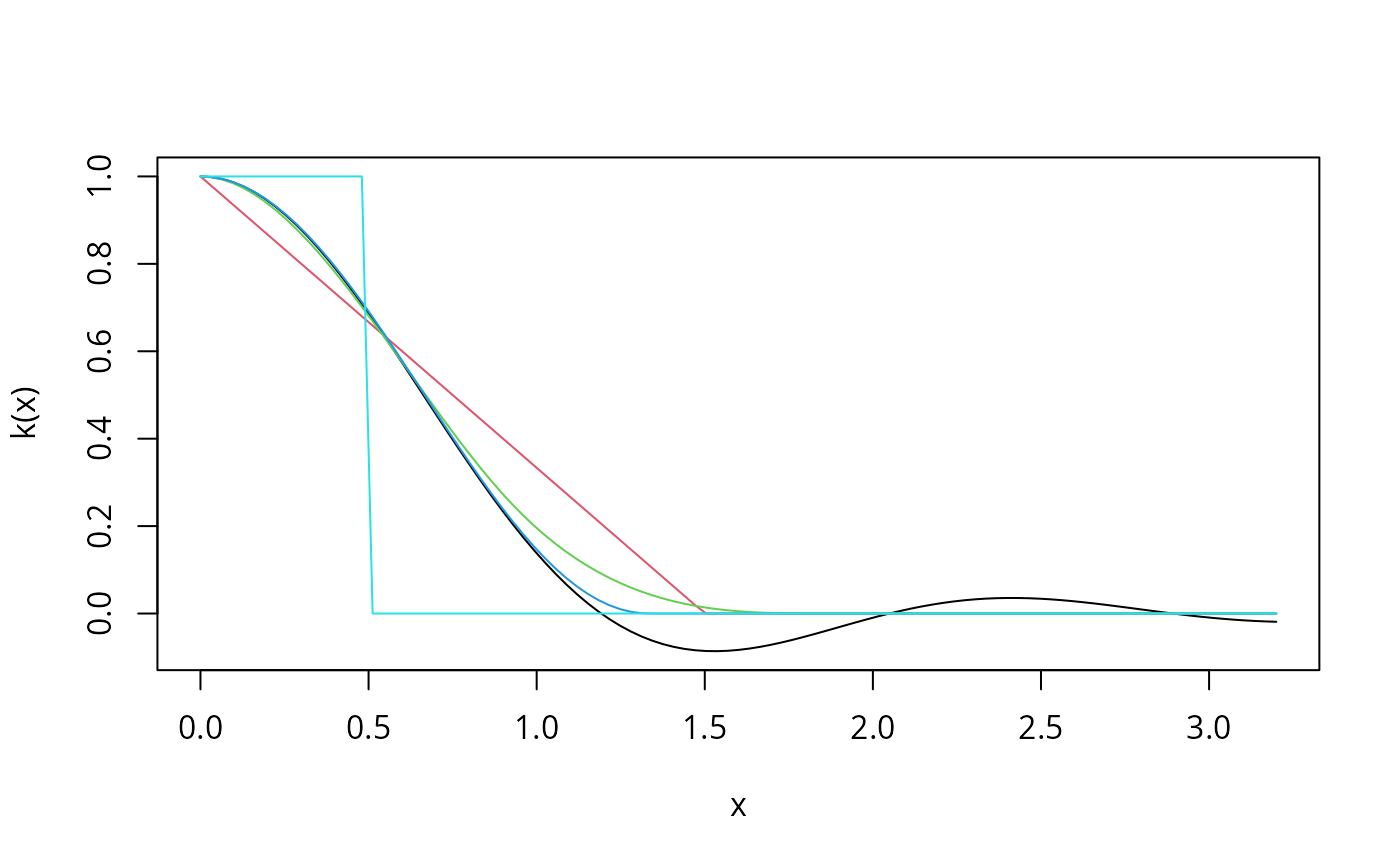

curve(kweights(x, kernel = "Quadratic", normalize = TRUE),

from = 0, to = 3.2, xlab = "x", ylab = "k(x)")

curve(kweights(x, kernel = "Bartlett", normalize = TRUE),

from = 0, to = 3.2, col = 2, add = TRUE)

curve(kweights(x, kernel = "Parzen", normalize = TRUE),

from = 0, to = 3.2, col = 3, add = TRUE)

curve(kweights(x, kernel = "Tukey", normalize = TRUE),

from = 0, to = 3.2, col = 4, add = TRUE)

curve(kweights(x, kernel = "Truncated", normalize = TRUE),

from = 0, to = 3.2, col = 5, add = TRUE)

## fit investment equation

data(Investment)

fm <- lm(RealInv ~ RealGNP + RealInt, data = Investment)

## compute quadratic spectral kernel HAC estimator

kernHAC(fm)

#> (Intercept) RealGNP RealInt

#> (Intercept) 788.6120652 -0.7502080996 49.78912814

#> RealGNP -0.7502081 0.0007483977 -0.06641343

#> RealInt 49.7891281 -0.0664134303 17.71735491

kernHAC(fm, verbose = TRUE)

#>

#> Bandwidth chosen: 1.744749

#> (Intercept) RealGNP RealInt

#> (Intercept) 788.6120652 -0.7502080996 49.78912814

#> RealGNP -0.7502081 0.0007483977 -0.06641343

#> RealInt 49.7891281 -0.0664134303 17.71735491

## use Parzen kernel instead, VAR(2) prewhitening, no finite sample

## adjustment and Newey & West (1994) bandwidth selection

kernHAC(fm, kernel = "Parzen", prewhite = 2, adjust = FALSE,

bw = bwNeweyWest, verbose = TRUE)

#>

#> Bandwidth chosen: 2.814444

#> (Intercept) RealGNP RealInt

#> (Intercept) 608.3101258 -0.5089107386 -64.93690203

#> RealGNP -0.5089107 0.0004340803 0.04689293

#> RealInt -64.9369020 0.0468929322 15.58251456

## compare with estimate under assumption of spheric errors

vcov(fm)

#> (Intercept) RealGNP RealInt

#> (Intercept) 620.7706170 -0.5038304429 8.47475285

#> RealGNP -0.5038304 0.0004229789 -0.01145679

#> RealInt 8.4747529 -0.0114567949 5.61097245

## fit investment equation

data(Investment)

fm <- lm(RealInv ~ RealGNP + RealInt, data = Investment)

## compute quadratic spectral kernel HAC estimator

kernHAC(fm)

#> (Intercept) RealGNP RealInt

#> (Intercept) 788.6120652 -0.7502080996 49.78912814

#> RealGNP -0.7502081 0.0007483977 -0.06641343

#> RealInt 49.7891281 -0.0664134303 17.71735491

kernHAC(fm, verbose = TRUE)

#>

#> Bandwidth chosen: 1.744749

#> (Intercept) RealGNP RealInt

#> (Intercept) 788.6120652 -0.7502080996 49.78912814

#> RealGNP -0.7502081 0.0007483977 -0.06641343

#> RealInt 49.7891281 -0.0664134303 17.71735491

## use Parzen kernel instead, VAR(2) prewhitening, no finite sample

## adjustment and Newey & West (1994) bandwidth selection

kernHAC(fm, kernel = "Parzen", prewhite = 2, adjust = FALSE,

bw = bwNeweyWest, verbose = TRUE)

#>

#> Bandwidth chosen: 2.814444

#> (Intercept) RealGNP RealInt

#> (Intercept) 608.3101258 -0.5089107386 -64.93690203

#> RealGNP -0.5089107 0.0004340803 0.04689293

#> RealInt -64.9369020 0.0468929322 15.58251456

## compare with estimate under assumption of spheric errors

vcov(fm)

#> (Intercept) RealGNP RealInt

#> (Intercept) 620.7706170 -0.5038304429 8.47475285

#> RealGNP -0.5038304 0.0004229789 -0.01145679

#> RealInt 8.4747529 -0.0114567949 5.61097245